Many banks require a minimum of 10 percent down; nevertheless, Bond recommends putting down a minimum of 20 percent to prevent paying personal home mortgage insurance coverage. Private mortgage insurance coverage is default insurance coverage payable to a loan provider, and it can include a couple of hundred dollars to your regular monthly home mortgage. Furthermore, recurring payments such as home loans, charge card payments, auto loan, and kid support, are used to determine your financial obligation to income ratio (DTI).

If you make $18,000 a month, your DTI would be 33 percent which falls within the variety where a bank would provide. The mistake of not having a credit rating is one barrier that might stop or delay the application procedure. According to Miller, just using a debit card can assist you start to establish a credit report.

The loan provider examines your work history, task stability, and down payment when determining whether you have the capability to pay back. "If you have actually been on your very first job for a month, you might wish to offer yourself a little time to develop a cost savings before leaping right into a home mortgage," says Miller.

Do your research to find a mortgage loan officer that comprehends your household goals and goals; somebody who can be a resource throughout the entire home loan procedure - what credit score do banks use for mortgages. Consumer Affairs is a fantastic location to start; the publication offers countless evaluations for dozens of different financing companies. Determining your debt-to-income ratio and understanding just how much of a monthly home loan payment you can manage will keep you from overextending yourself and becoming "home bad.".

Numerous or all of the products featured here are from our partners who compensate us. This may influence which items we compose about and where and how the product appears on a page. Nevertheless, this does not affect our assessments (what is the current index for adjustable rate mortgages). Our viewpoints are our own. You've decided to purchase a home.

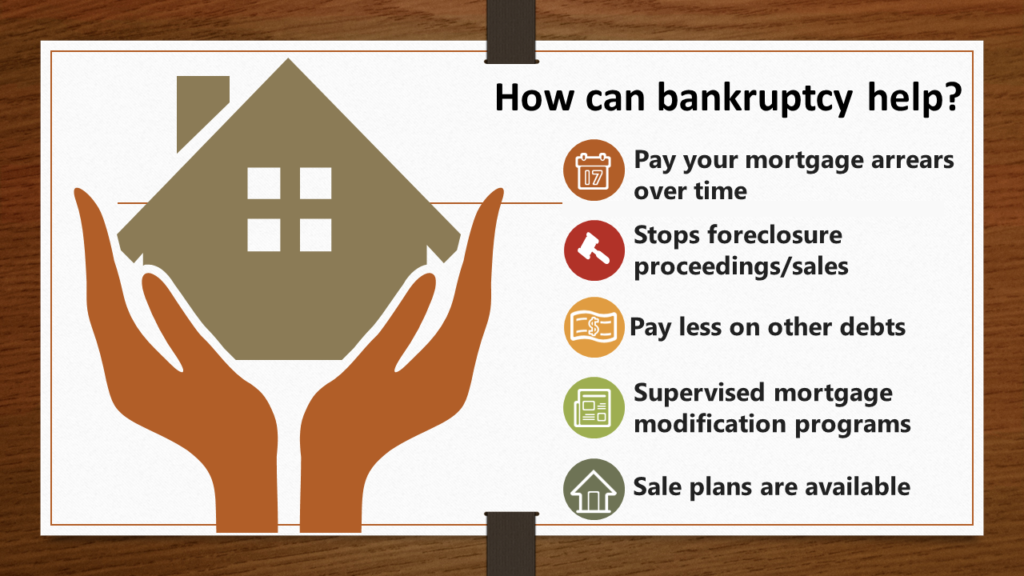

More About What Is The Catch With Reverse Mortgages

Take a big breath it's not every day you make an application for a loan with that many zeros. Preparation is crucial, since after your purchase deal is accepted, the clock is ticking. Closing a home mortgage deal takes about 45 days typically. "If you enter into the process without [the proper] details, it might slow you down," says Randy Hopper, a vice president at Navy Federal Credit Union.

Now that you have actually made an offer on a house, it's time to pick the finalist that you will actually obtain the cash from. Start by telephoning loan providers (three, at minimum), visiting their workplaces or submitting their mortgage applications online. Most convenient of all: Ask an agent to fill out the form while you fill out by phone or personally, says Carlos Miramontez, vice president of home loan loaning at Orange County's Cooperative credit union in California.

Mark Burrage, USAA "If you want to start online, and you specify where you require more details or simply wish to talk with a live human being, the vast majority of lending institutions are set up to where you can transport switch," states Mark Burrage, an executive director for USAA.

And your credit history will not struggle with submitting multiple applications as long as you send them all within a 45-day window. You need to constantly submit multiple applications so you can compare deals later. It's an excellent concept to employ a home inspector to assess the residential or commercial property's condition right away, despite the fact that loan providers don't need it.

/can-you-transfer-a-mortgage-315698-v2-0ab571d8ed8e4f3dad681629e9ef8aeb.png)

This will cost around $300 to $500. The lenders ask authorization to pull your credit. By law, a lending institution has 3 organization days after getting your application to provide you a Loan Price quote kind, an in-depth disclosure showing the loan amount, type, rates of interest and all costs of the mortgage, including threat insurance, home mortgage insurance coverage, closing expenses and property tax.

What Are Lenders Fees For Mortgages - Questions

Now use your Loan Estimate forms to compare terms and costs. At the upper right corner of the very first page you'll see expiration dates for the rates of interest find out if it's "locked" and closing expenses. Ask the lending institution to describe anything you do not comprehend. If the numbers Visit website appear dizzying, "Don't focus too much on rate," Burrage states.

These will allow you to easily compare offers: This is all charges consisting of interest, principal and home loan insurance coverage that you'll sustain within the mortgage's very first 5 years. This is the amount of principal you'll have paid off in the very first five years. Also known as its annual percentage rate. This is the portion of the loan paid in interest over the whole life of the home loan.

The loan provider's job is to answer all your concerns. If you can't get good responses, keep shopping. [Back to top] You've compared lending institutions' rates and charges. Now examine their responsiveness and credibility. Reconsider anybody who makes you feel forced, Burrage states. His recommendations: "Go with someone you can trust." Then call the loan provider of your choice to state you're ready to continue.

[Back to top] Every declaration you made on your mortgage application goes under the microscopic lense in this phase. Brace for concerns and file demands. Reacting immediately keeps everything progressing. You stated you make $50,000 annually at Acme Software? The processor looks at your pay stubs and calls Acme's HR department to validate.

[Back to top] Your job now is to stand by. If you're required at all, it will be to answer more concerns and produce more documents. The underwriter's task is to evaluate the danger of providing money to you on this property. What's your loan-to-value ratio? Do you have the money circulation to make the regular monthly payments? How about your "credit character"? What's your history of making payments on time? Is the house valued properly, the condition excellent and title clear? Is it in a flood zone? [Back to top] In this last step, the lending institution needs to act getting rid of timeshare maintenance fees before the debtor can progress.

How Do Reverse Mortgages Really Work Fundamentals Explained

It reveals the detailed and last expenses of your home mortgage. Analyze the Closing Disclosure read more carefully to compare it against the Loan Quote type to see if any of the priced estimate fees or numbers have actually changed. If they have, ask the lending institution to explain. Compare the Closing Disclosure with your Loan Estimate to see if any of the priced quote fees or numbers have altered.

[Back to top] This is the moment to choose if you wish to proceed. If you do, you're on to your closing, with, yes, one last mountain of documentation to sign. However it'll quickly be over. You have actually completed the mortgage application marathon and declared your shiny brand-new loan. Well done.

Fixed-rate or adjustable-rate mortgage? To escrow or not to escrow? Pre-qualification vs. pre-approval? Home loan financing can appear confusing, but it doesn't have to be. There are a couple of key things to comprehend, and the more you understand, the more prepared you'll be. Type of loan that is protected by property (i.

Unless you are paying money for the home, you'll need a home mortgage. You guarantee to pay back the lending institution (usually in regular monthly payments) in exchange for the cash utilized to buy the house. If you stop paying, you'll go into default, which indicates you've failed to fulfill the terms of the loan and the lender can reclaim the property (foreclosure).